Is Home Insurance Really Necessary? A Breakdown for Renters and Owners

Protecting Your Home: Understanding Home Insurance in Canada for Renters and Owners

For many, a home is their most valuable asset, whether they own it or rent it. While often overlooked or seen as an unnecessary expense, home insurance in Canada is a critical component of financial protection and peace of mind. It safeguards your belongings and your liability against unforeseen events. This guide will break down the necessity of home insurance, distinguishing between policies for renters and owners, and explaining what they typically cover.

Why is Home Insurance Necessary?

Home insurance provides financial protection against a wide range of risks. Without it, you could face significant financial losses due to:

- Property Damage: Fire, theft, vandalism, water damage (burst pipes).

- Liability: If someone is injured on your property and you are found responsible.

- Loss of Use: Covers additional living expenses if your home becomes uninhabitable due to a covered peril.

Important: While not legally mandatory in all provinces, most mortgage lenders require homeowners to have insurance. Landlords often require tenants to have renter's insurance.

Renter's Insurance (Tenant Insurance)

Renter's insurance protects your personal belongings and provides liability coverage. It does NOT cover the building itself, as that is the landlord's responsibility.

What Renter's Insurance Typically Covers:

- Personal Property: Covers your belongings (furniture, electronics, clothing, jewelry) against specified perils like fire, theft, and water damage, whether they are in your home or temporarily elsewhere (e.g., in your car, at a storage unit).

- Liability: Protects you if someone is injured in your rental unit and you are found legally responsible. It also covers damage you accidentally cause to the building (e.g., a kitchen fire).

- Additional Living Expenses: If your rental unit becomes uninhabitable due to a covered event, it covers the cost of temporary accommodation and food.

Why it's Essential for Renters:

Many renters mistakenly believe their landlord's insurance covers their personal belongings. It does not. Without renter's insurance, you would have to replace everything out of pocket if a fire or theft occurred. The liability coverage is also crucial for protecting your financial future.

Homeowner's Insurance

Homeowner's insurance is a comprehensive policy that protects the structure of your home, your personal belongings, and provides liability coverage.

What Homeowner's Insurance Typically Covers:

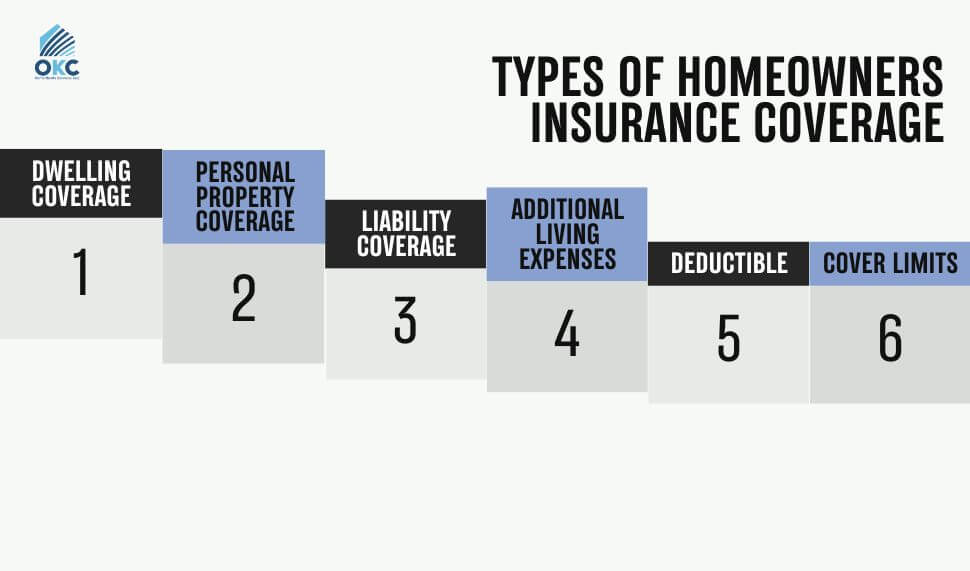

- Dwelling: Covers the physical structure of your home (walls, roof, foundation) against specified perils.

- Detached Structures: Covers garages, sheds, and fences on your property.

- Personal Property: Covers your belongings, similar to renter's insurance.

- Liability: Protects you if someone is injured on your property or if you accidentally cause damage to someone else's property.

- Additional Living Expenses: Covers costs if you need to live elsewhere while your home is being repaired after a covered loss.

Types of Homeowner's Policies:

- Basic/Named Perils: Covers only the risks specifically listed in the policy (e.g., fire, theft, windstorm).

- Broad Form: Covers all perils for the dwelling and detached structures, but only named perils for personal property.

- Comprehensive/All Perils: Covers all perils for both the dwelling and personal property, except for those specifically excluded (e.g., flood, earthquake, nuclear war). This is the most common and recommended type.

The cost of your home insurance policy is influenced by several factors:

- Location: Crime rates, proximity to fire hydrants/fire stations.

- Type of Home: Age, construction materials, roof type.

- Claims History: Your past insurance claims.

- Deductible: The amount you pay out of pocket before your insurance kicks in. A higher deductible usually means lower premiums.

- Security Features: Alarms, deadbolts, smoke detectors.

- Credit Score: In some provinces, your credit score can influence your insurance premiums.

How to Get Home Insurance

You can obtain home insurance through:

- Insurance Brokers: Independent professionals who can compare quotes from multiple insurance companies.

- Direct Writers: Insurance companies that sell policies directly to consumers (e.g., TD Insurance, Desjardins).

- Banks: Some banks offer insurance products.

It's always recommended to get multiple quotes and compare coverage before making a decision.

Conclusion: Essential Protection for Your Canadian Home

Whether you're renting or owning, home insurance is not just an option; it's an essential layer of financial protection in Canada. It safeguards your belongings, protects you from liability, and provides peace of mind. By understanding the differences between renter's and homeowner's policies and choosing the right coverage, you can ensure your home and your financial future are secure in your new Canadian life.

Related content